By Anurag Sharma

The Hidden Risk Behind a "Comfortable" LLCR

A major real estate company was in the final stages of raising debt. Their CFO, had full confidence in the internal team. His team had built the financial model themselves, weeks of work, multiple iterations, late nights refining every sheet. By the time they reached lender discussions, they knew the model inside out.

On one of the final calls, he said it clearly:

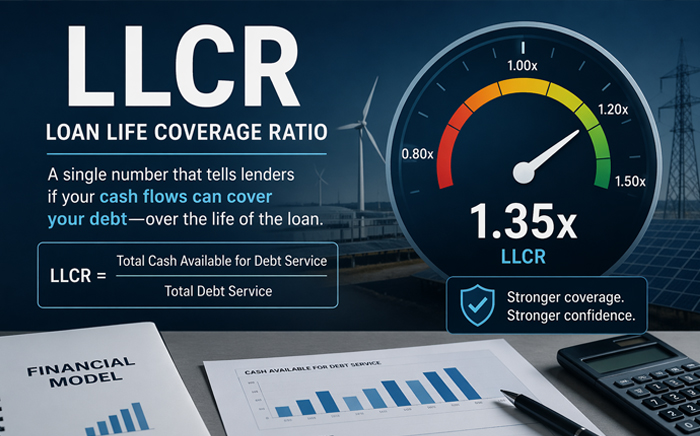

“Our LLCR is 1.35x. We’re comfortable with the coverage.”

The lenders seemed satisfied. The conversation moved on. The deal was progressing smoothly.

Then, just before closing, one of the lenders asked:

“What assumptions are actually driving that number?”

There was a pause.

Not because they didn’t have the answer, but because they hadn’t really broken it down that way. The number was there. The model worked. That had been enough.

On the surface, everything looked perfect.

But when they started digging deeper, small things began to surface.

None of these broke the model. And so it still showed: LLCR = 1.35x

The deal closed.

A few months into operations, things started to feel tighter than expected. Cash wasn’t behaving the way the model had suggested.

They went back to the model. This time, they looked deeper.

There were still no broken cells. No obvious errors.

Just small distortions, the kind that quietly pass through every check.

Together, they added up to one thing:

LLCR had been overstated by 0.10x

It didn’t break the deal. But it changed everything:

Looking back, the model hadn’t failed.

That was exactly the problem.

Because LLCR isn’t just a ratio. It’s the entire model assumptions, timing and structuring, compressed into a single number. And when that number looks clean, it’s easy to trust it without questioning it.

The real mistake wasn’t calculating LLCR.

It was not asking:

“Is this LLCR telling the truth?”

That experience changed how they approached models.

“Next time, we won’t rely only on internal comfort. We’ll bring in an independent lens.”

Because in project finance, the biggest risks not only comes from broken models

They come from models that look working perfectly.

That’s where teams like EMF come in, not only to fix errors, but to ensure the model is actually telling the truth.

On one of the final calls, he said it clearly:

“Our LLCR is 1.35x. We’re comfortable with the coverage.”

The lenders seemed satisfied. The conversation moved on. The deal was progressing smoothly.

Then, just before closing, one of the lenders asked:

“What assumptions are actually driving that number?”

There was a pause.

Not because they didn’t have the answer, but because they hadn’t really broken it down that way. The number was there. The model worked. That had been enough.

On the surface, everything looked perfect.

- No broken formulas

- No Excel errors

- All checks passing

But when they started digging deeper, small things began to surface.

- Cash flows extending slightly beyond loan maturity

- Discounting not fully aligned with the term sheet

- Reserve balances being counted more than once

- Timing mismatches between CFADS and debt

None of these broke the model. And so it still showed: LLCR = 1.35x

The deal closed.

A few months into operations, things started to feel tighter than expected. Cash wasn’t behaving the way the model had suggested.

- Distributions slowed

- Covenant headroom narrowed

- Cash buffers felt thinner

They went back to the model. This time, they looked deeper.

There were still no broken cells. No obvious errors.

Just small distortions, the kind that quietly pass through every check.

Together, they added up to one thing:

LLCR had been overstated by 0.10x

It didn’t break the deal. But it changed everything:

- Less cushion than we believed

- Tighter lender position

- Delayed equity distributions

Looking back, the model hadn’t failed.

That was exactly the problem.

Because LLCR isn’t just a ratio. It’s the entire model assumptions, timing and structuring, compressed into a single number. And when that number looks clean, it’s easy to trust it without questioning it.

The real mistake wasn’t calculating LLCR.

It was not asking:

“Is this LLCR telling the truth?”

That experience changed how they approached models.

“Next time, we won’t rely only on internal comfort. We’ll bring in an independent lens.”

Because in project finance, the biggest risks not only comes from broken models

They come from models that look working perfectly.

That’s where teams like EMF come in, not only to fix errors, but to ensure the model is actually telling the truth.